{kind=link}

Local Lodging Taxes in Minnesota

Lodging taxes are imposed on short-term lodging by a number of local governments in Minnesota, mainly by cities and towns. All cities and towns, and counties on behalf of unorganized townships, may impose up to a 3 percent tax by statute, if 95 percent of the revenue raised is used for tourism promotion. Lodging taxes imposed at a higher rate or for other purposes are generally imposed under special law, although a few enacted before 1972 were imposed by city charter.

This information brief provides a history of local lodging taxes in Minnesota. In addition to the history, a table at the end provides more detail on the local lodging taxes imposed by special law or city charter by individual local governments.

Lodging Taxes Prior to 1972

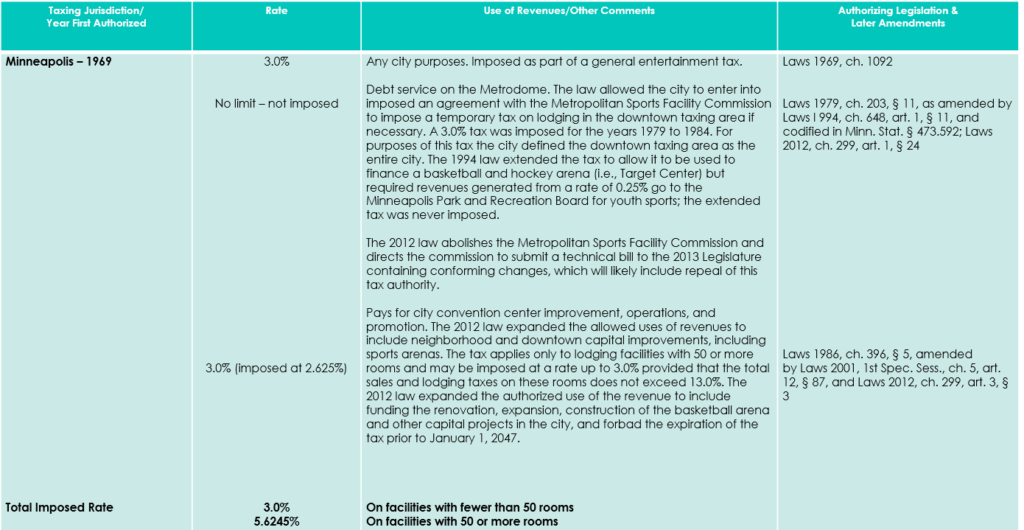

Prior to 1972, the state did not prohibit local governments from imposing local sales taxes on either general sales or sales of specific items, including lodging. Home rule charter cities could enact local lodging taxes if allowed under the charter. In 1969 a special law was passed that allowed Minneapolis to impose a 3 percent tax on admissions, transient lodging, and sales at restaurants and bars with live entertainment.

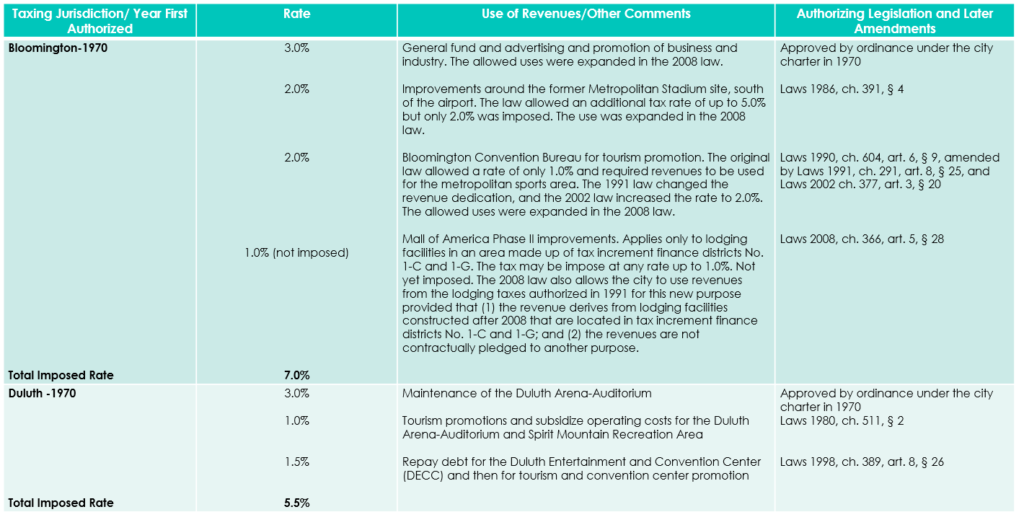

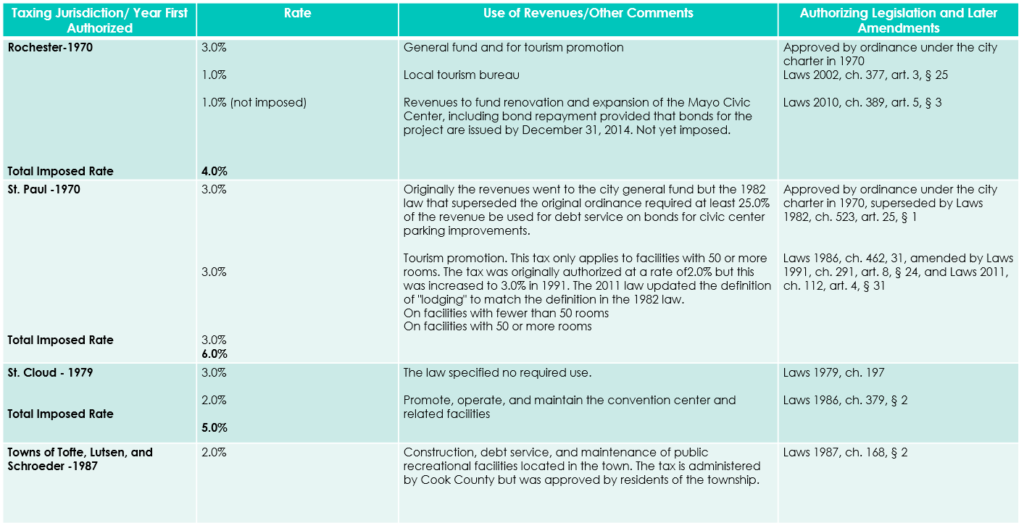

In 1970, Bloomington, Duluth, and St. Paul all passed 3 percent transient lodging taxes by ordinance and charter amendments. The Bloomington tax also applied to admissions to spectator events. In 1971, the city of Rochester also adopted a 3 percent local lodging tax by charter amendment and ordinance.

Prohibition Against Most Local Taxes in 1971

In 1971, as part of the “Minnesota Miracle” and as a tradeoff for more state aid to local governments, the legislature enacted a general prohibition against new or increased local sales and income taxes. The law states that ”No county, city, town, or other taxing authority shall increase a present tax or impose a new tax on sales or income.”1 This prohibition applies to lodging taxes as well as general sales taxes. The preexisting taxes, however, were allowed to continue.

Between 1972 and 1983 only two new lodging taxes were authorized under special law: a 3 percent tax in the city of St. Cloud ( 1979) and a Minneapolis tax ( 1979) in the downtown area to fund the Metrodome. 2

General Statutory Authority for Lodging Taxes

In 1983, notwithstanding the general prohibition against local sales taxes, the state authorized cities to impose a local sales tax of up to 3 percent on transient lodging of 30 days or less. 3 In 1985 the authority was expanded to towns and counties on behalf of unorganized territories in the county. The authority was also granted to any combination of cities, towns, and counties acting under a joint powers agreement. In addition, the 1985 law allowed cities to extend the lodging tax on camping site receipts in a municipal campground. Currently, about 100 jurisdictions impose a local lodging tax under this authority.

A city can impose the tax by ordinance, and a town can impose the tax by a vote of the electors at a general or special town meeting. To impose the tax in unorganized territories, the county board must pass a resolution to that effect, put a public notice in the newspaper, and hold a public hearing prior to passing a final resolution imposing the tax. If 5 percent of the voters in the unorganized territories petition for a vote within 30 days of the final resolution, the tax may not be imposed until approved by the voters in the unorganized territories at a general or special election.

Ninety-five percent of the revenues from a tax imposed under the general authority must be used for tourism and convention center promotion. In addition, the statute prohibits a local government that has a lodging tax imposed by a special law or charter provision to use the statutory authority to increase the combined lodging tax rate to more than 3 percent.

In 1987, as part of the recodification of the local lodging tax statute, a provision was added allowing a jurisdiction to negotiate with the Department of Revenue to collect the lodging tax. The department is allowed to retain from the collected revenues an amount to cover the costs of collection. Most local governments continue to collect the tax locally; the state only collects lodging tax for the cities of Minneapolis, St. Paul, Rochester, and Biwabik. A 2011 law requires that any local lodging tax collected by the state to use the statutory definition of “lodging” in chapter 297 A as the tax base. The current definition of lodging contained in Minnesota Statutes, section 469 .190, differs slightly from the definition for sales tax purposes contained in Minnesota Statutes, section 297A.61, subdivision 3, paragraph (g), clause (2), as do the lodging definitions for lodging taxes imposed under some of the special laws.

During the 1989 special session, the law was amended to increase the maximum local lodging tax rate imposed under the statute from 3 percent to 6 percent and to allow the local government to use the amount raised by the tax rate above 3 percent for general governmental purposes. This increase in authority was repealed in 1990, and the allowed rate of 3 percent and allowed use for tourism and convention promotion have not changed since 1990.

Use of Local Sales Tax Revenue for First Class Cities

In Laws 2012, chapter 299, article 5, section 6, all cities of the first class were granted additional flexibility in the use of revenue derived from any local sales tax, including lodging taxes.5 A city may divert any revenue not needed to fund the projects listed in the authorizing law for the local tax to fund construction, expansion, or renovation projects for a sports facility or convention center, if the project cost is at least $40 million.

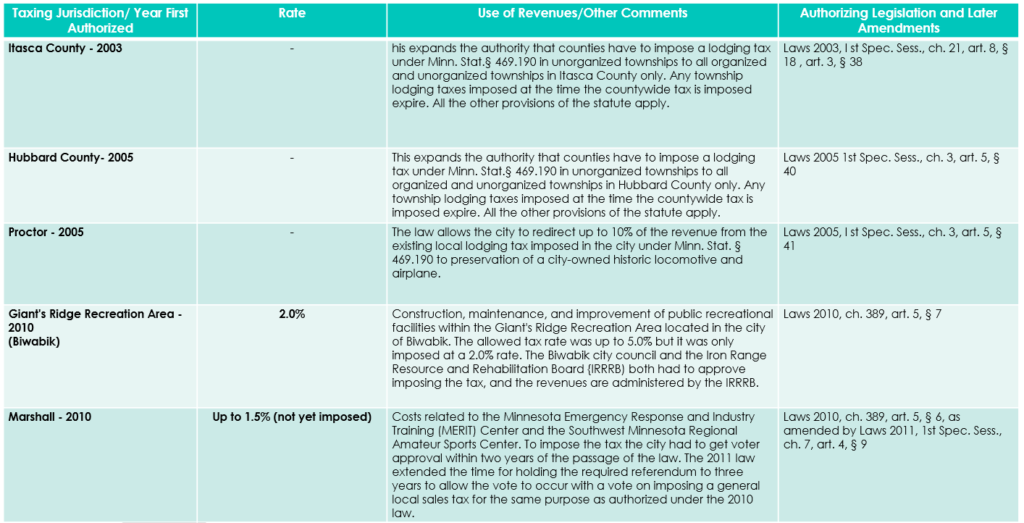

A summary of the lodging taxes imposed under special law, or by local charter prior to 1972, are listed in the following table.

Copies of this publication may be obtained by calling 651-296-6753. This document can be made available in alternative formats for people with disabilities by calling 651-296-6753 or the Minnesota State Relay Service at 711 or 1-800-627-3529 (TTY). Many House Research Department publications are also available on the Internet at: www.house.mn/hrd/hrd.htm.

Website Design and Development by W.A. Fisher Interactive. Report Problems